Seller Credits vs. Price Reduction: Which Is Best for Colorado Luxury Home Sellers?

R Squared Realty Experts April 11, 2025

EXPERT ADVICE & KNOWLEDGE

R Squared Realty Experts April 11, 2025

EXPERT ADVICE & KNOWLEDGE

When you’re selling a high-value home in Colorado, you’ll inevitably face the question: Should I offer a seller credit or simply lower my asking price? It’s a strategic decision with real financial impacts, especially in the luxury market. In this blog, we’ll break down the pros and cons of offering seller concessions (credits) versus reducing the purchase price. We’ll use current Colorado housing data and clear examples to illustrate how each choice plays out – from average-priced homes to luxury properties. By the end, you’ll understand why many sellers (and builders) often prefer credits, how appraisals handle these concessions, what it means for your taxes, and how R Squared Realty Experts can guide you to the best outcome.

A strategic discussion with your real estate agent can help determine whether a seller credit or a price cut will best achieve your goals in Colorado’s housing market.

Colorado’s real estate market spans from modest starter homes to multi-million dollar estates. As of late 2024, the median single-family home price in the Denver metro area was around $600,000 – a record high driven in part by a surge in luxury sales recolorado.com. Statewide, typical home values hover in the mid-to-high $500,000s. In this “traditional” price range, it’s not uncommon for sellers to offer concessions (credits toward buyer costs) especially when buyer demand softens. In fact, depending on market conditions, anywhere from about 25% nar.realtor to nearly 45% mansionglobal.com of recent home sales have involved some form of seller concession.

Luxury homes (often defined as $1 million and above in Colorado) are a world of their own. In Denver’s high-end enclaves, median prices easily exceed $1.2 milliontrymasterkey.com. In these upscale segments, seller concessions have historically been less common – affluent buyers might not need help with closing costs, and in red-hot markets, sellers had little incentive to offer. However, with higher interest rates and more inventory in 2024-2025, even luxury sellers are now considering credits as a tool to attract buyers. The norm for concessions in Colorado is usually a few percent of the purchase price at most (often covering typical closing costs). For a median-priced home (~$600k), that might be a $5,000–$15,000 credit. For a $1.2 million luxury listing, a similar 2–3% concession could be $25,000–$35,000 or more – a sizeable perk for the buyer.

Before weighing the trade-offs, let’s clarify the terms:

Seller Credit (Concession): This is an amount the seller agrees to contribute toward the buyer’s closing costs or other expenses at closing. It’s essentially a financial incentive to the buyer. Commonly, credits are used to pay for things like loan origination fees, appraisal fees, title insurance, or to buy down the buyer’s mortgage interest rate. The credit is reflected on the closing statement, reducing the amount of cash the buyer must bring. Importantly, the home’s contract price remains the same. For example, a buyer offers $500,000 on a home with a $10,000 seller credit – the contract price stays $500k, but the buyer gets $10k worth of assistance from the seller at closing.

Price Reduction: This is a straight drop in the purchase price of the home. The buyer pays less, and the contract price is adjusted downward. For instance, rather than selling at $500,000, the seller might agree to lower the price to $490,000 instead of offering a credit. The buyer’s mortgage and down payment are based on this lower price, but the buyer then covers their own closing costs in full.

Both strategies mean less net money in the seller’s pocket, but they impact the transaction (and the perception of value) in different ways. Next, we’ll explore why many buyers – especially in today’s market – often prefer a seller credit over an equivalent price cut.

From a buyer’s perspective, seller credits can be far more valuable than a price reduction of the same amount. Here’s why:

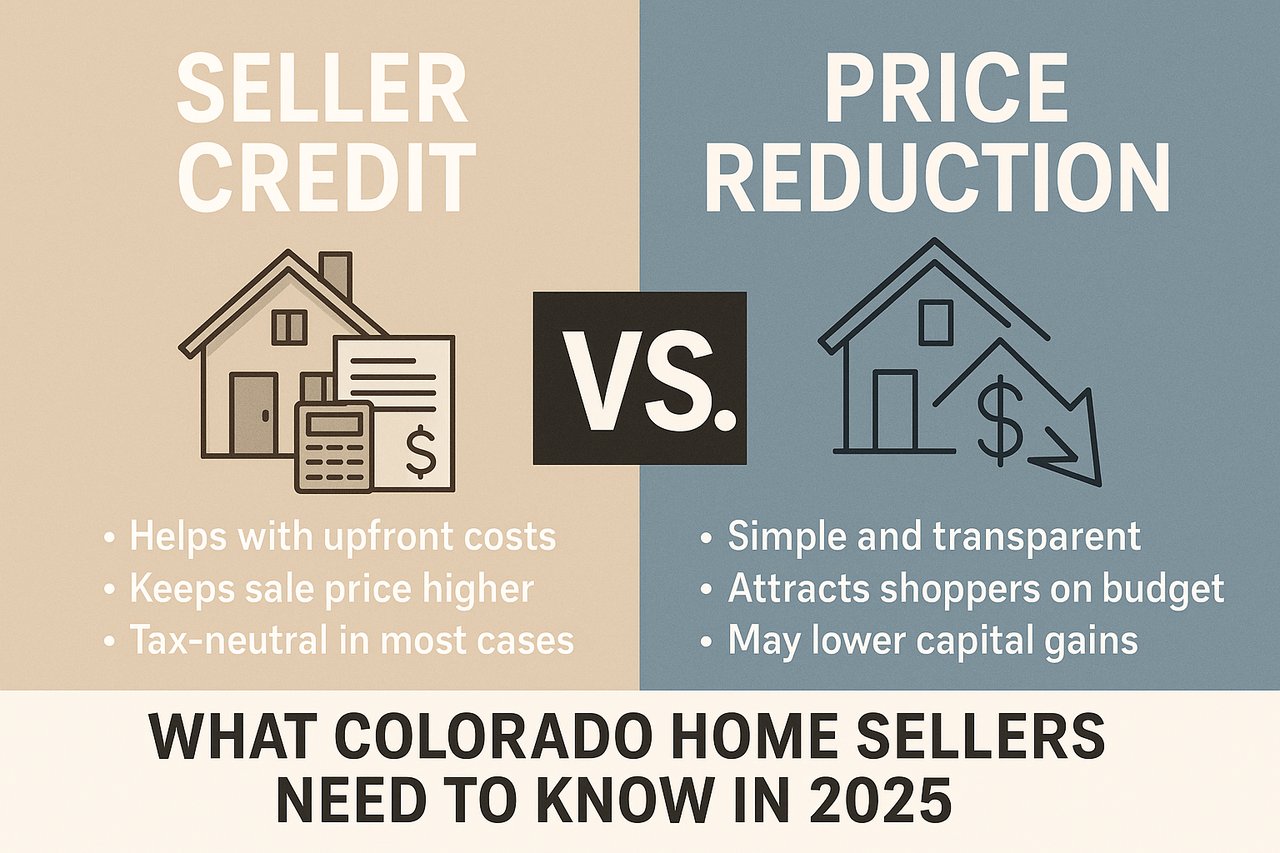

Helps with Upfront Costs: Buying a home involves significant upfront cash beyond just the down payment (loan fees, title fees, insurance, taxes, etc.). In Colorado, buyer closing costs typically range from about 2% to 5% of the purchase price prevu.com. On a $600,000 home, that could be $12,000–$30,000 due at closing! A seller credit that covers, say, $15,000 of closing costs dramatically reduces the cash the buyer must bring to the table. In contrast, a $15,000 price reduction only lowers the down payment and loan amount slightly – it doesn’t put cash in the buyer’s hand for those extra fees.

Interest Rate Buy-Downs: In today’s higher interest rate environment, buyers are very sensitive to monthly payments. One popular use of seller credits is to buy down the mortgage rate. For example, a seller offering a credit of $20,000 can allow the buyer to purchase discount points and lower their interest rate, perhaps from 7% to 6.5%, on a large loan. The effect on the buyer’s monthly payment is significant – often more than if the buyer simply paid a slightly lower price for the home. In other words, a credit can reduce the buyer’s monthly payment more effectively than a price drop of the same size. (We’ll see a clear example of this in the $1.2M scenario below.)

Eases the Move-In Burden: Credits can also be applied to other expenses like prepaid homeowners insurance, property taxes, or even HOA fees. This flexibility means a buyer can walk into their new home with more money in their pocket, or a more affordable mortgage, as a result of the credit. A price reduction, on the other hand, primarily benefits the buyer long-term (slightly lower loan balance and maybe a marginally lower tax basis), but it doesn’t help them today with the hefty cash required to close.

Psychological Incentive: Seeing an offer of “$$$ towards closing costs!” often motivates buyers more than an equivalent price tweak. It feels like getting help or a bonus. Many buyers, especially first-timers or those stretching for a luxury home, will choose the house that offers a credit over one that simply had a small price cut, because the immediate relief is greater.

Crucially, offering a credit does not cheapen the perceived value of the property – the list price remains intact. This brings us to a key point: how keeping a higher price (with a credit behind the scenes) can actually protect the value of your home and your neighbors’ homes.

One major advantage of a seller credit is that it preserves the official sale price of your home, which can be important for both appraisal and neighborhood comp purposes:

Neighborhood Comparables: Colorado homeowners care about their property values. If you sell your house for $25,000 less, that lower price becomes a new data point (“comp”) that appraisers and future buyers in the area may look at. Multiple price-reduced sales can nudge values downward. In contrast, if you sell at full price with a concession, the recorded sale price in the MLS and public records doesn’t reflect the credit. You’ll still be noted as having sold at $1.2M instead of $1.175M, for example. This helps maintain higher neighborhood comps because the sale appears stronger. (Even developers use this tactic – many new-home builders prefer to offer incentives like paying closing costs rather than cut their base prices, specifically to keep values high mansionglobal.com.)

Appraisal Treatment: While the sale price recorded stays high with a credit, appraisers will still take concessions into account when evaluating market value. Per industry guidelines, an appraiser compares each comparable sale’s terms to determine if a seller concession likely inflated the price kairosappraisal.com. For example, if a comparable home sold for $455,000 with a $5,000 credit, the appraiser might judge that it would have sold for only $450,000 without that creditkairosappraisal.com. In such case, they may adjust that comp down by the $5,000 to reflect a true market price. On the other hand, a home that sold for $440,000 with a $5,000 credit (net $435k) might be considered just a normal negotiation, not requiring adjustmentkairosappraisal.com. The key is whether the concession was outside the norm for the market.

In luxury price brackets, this issue can be magnified. Fewer comparable sales exist, and if one sale included an unusually large concession, an appraiser might question if the contract price was artificially high. Lenders also have limits (often 3% to 6% of price) on how big a credit can be for a given loan productcoloradokeyrealestate.com. Fortunately, most credits – even $25k on a $1.2M sale (~2%) – are within normal ranges and viewed as part of standard negotiations. As long as concessions in your area are common (and lately they are), appraisers in Colorado typically treat a reasonable seller credit as not diminishing the home’s intrinsic value. They will note it in the appraisal report, but if it aligns with market norms, it usually won’t derail the appraisal. This means you get the best of both worlds: the home appraises at (or near) the full contract price, and you’ve helped the buyer with costs without eroding the perceived value.

Future Sales & Refinances: By keeping the sale price higher, you also help maintain values for future transactions. If you’re selling a luxury home in, say, Cherry Creek, you probably don’t want to be the one sale that undercuts the $1.2M neighborhood benchmark. Likewise, your buyer (if they know the market) may appreciate that the home’s value isn’t “marked down” in public perception – it could matter when they go to sell or refinance. In short, credits help protect the integrity of pricing in the area, whereas widespread price reductions could chip away at the market’s overall appraisal benchmarks.

From the seller’s perspective, money is money – a $25,000 credit or a $25,000 price drop both reduce your proceeds by the same amount. However, there are some nuanced pros and cons to consider for each approach beyond just the sale price:

Seller Credits – Advantages:

Attract a Wider Buyer Pool: Advertising a seller credit (for closing costs or rate buy-down) can draw in buyers who might otherwise be unable to afford the upfront costs. This is especially helpful in the luxury segment where buyers may have substantial incomes but are cautious about cash flow. Your listing stands out as more affordable to close, which can lead to more offers and a faster sale.

Maintain Higher Net Price for Comps: As discussed, you keep the top-line price high, supporting both your home’s value and broader neighborhood values. This can be a strategic move in a softer market to avoid “dragging down” pricing in your area.

Buyer Perceives More Value: A buyer getting, say, “$25,000 towards closing costs” feels like they’ve gotten a deal. They might be willing to offer closer to your asking price because they plan to recoup some cash at closing. In contrast, if you simply cut the price upfront, the buyer may still negotiate you down further and ask for repairs or other concessions later. A credit can sometimes satisfy a buyer’s request for a “deal” without further eroding your price.

Tax-Neutral in Most Cases: From a tax standpoint, a seller credit typically reduces your net proceeds, just like a price reduction. The IRS generally treats credits as a reduction in the amount you realize from the sale (similar to paying a closing cost on the sale) – so it should not increase your capital gains liabilityweloveyourtaxes.com. For example, if you sell for $1.2M with a $25k credit, effectively you net $1.175M. You’d likely be taxed as though you sold for $1.175M. (Always confirm with your accountant, but in principle you won’t be penalized for choosing a credit over a lower price.)

Seller Credits – Disadvantages:

You Pay Costs (and Commission on the Full Price): A credit comes out of your proceeds, which means you are essentially writing a check for the buyer at closing. You’ll also pay REALTOR® commission based on the full contract price. Using the earlier example, if you agreed to 5% commission, a $1.2M price with $25k credit means commission on the full $1.2M (which is $60,000 at 5%). Had you simply sold for $1.175M, commission would be $58,750. That’s a modest difference, but it’s worth noting – offering a large credit can cost a bit more in feessince those are percentage-based.

Limits and Appraisal Scrutiny: Extremely large credits can raise eyebrows. Lenders usually cap credits (for instance, a conventional loan with 20% down allows up to 6% of the price in credits boulderhomesource.com). If you offer more than the allowable amount, the excess can’t be used by the buyer – essentially forcing a price cut anyway. Additionally, if credits are uncommon in your sub-market and you’re the only seller giving one, an appraiser might adjust the value slightly. However, in most of Colorado’s current market, this is a minor risk given how common concessions have become.

Perception by Some Buyers: While many buyers love credits, a few might be skeptical. A very large credit could signal to a buyer that your price is high or that the home may have trouble (why else would the seller “give” so much?). This is usually mitigated by proper explanation (“The credit is to help buy down your rate, given interest rates right now”), but it’s something your agent will navigate in negotiations.

Price Reduction – Advantages:

Simplicity and Transparency: There’s something clean and straightforward about just lowering the price. All parties see it, and there’s no special stipulation in the contract about a credit. For sellers who like to keep things simple, a price cut is easy to understand.

May Attract Price-Conscious Shoppers: If your home is just above a pricing threshold (say $605k, and dropping to $585k puts it under a mental cutoff), a price reduction can expose your listing to a new set of buyers. In the luxury range, dropping from $1.05M to $999k, for instance, can be a game-changer for visibility. A credit, conversely, is often invisible until negotiations – it won’t show up in an online search filter.

Slight Relief on Commissions/Taxes: A lower sale price means slightly lower commission paid and, possibly, lower capital gains if your profit exceeds the tax-free limit. Luxury sellers should note: if you have a large gain beyond the $250k (single) or $500k (married) IRS exclusion weloveyourtaxes.com, every $1 you don’t collect is $1 less to potentially be taxed. Taking $25k off the price could save you a few thousand in capital gains tax (15–20% on that $25k, if your gain isn’t excluded). With a credit, as long as it’s treated as reducing your proceeds, you’d have a similar tax result – but you want to be sure it’s documented correctly. In short, a price reduction automatically locks in that tax benefit of a lower price.

Price Reduction – Disadvantages:

Less Enticing to Buyers Needing Cash: A price drop might not solve a buyer’s biggest hurdle: upfront cash. For instance, reducing your $1.2M price by $25k only lowers a 20% down payment by $5k. The buyer might still be struggling to cover $50k+ in closing and moving costs. So a price cut could fall flat as an incentive, whereas offering to pay, say, their $25k in closing expenses directly addresses their pain point.

Lower Recorded Value: The flip side of the comp discussion – your home will now be on record as selling for less. This could subtly impact the perceived market value. If multiple high-end homes in your neighborhood start selling for under list due to price cuts, appraisers will note that trend. You could be contributing to a market cooldown that might affect you (if you’re selling another property later) or your neighbors. While each situation differs, many Colorado luxury sellers prefer not to be the ones setting a “low water mark” with a big price drop.

“Am I Leaving Money on the Table?”: Sellers often wonder if they reduce the price too quickly or by too much. A credit can be targeted (cover specific buyer needs) and only applied if the deal actually closes, whereas a price reduction is a public move that can’t be taken back if a buyer would have paid more. In a scenario where a buyer would have been happy with a credit, you, as the seller, might unnecessarily give up extra value by choosing a price cut. It’s about efficiency: $1 in credit can sometimes yield more buyer happiness than $1 in price reduction.

In summary, seller credits typically provide more bang for your buck in enticing buyers, without dragging down property values – but they require the seller to foot certain bills for the buyer. Price reductions are straightforward and can broaden your market audience, but much of their benefit accrues to the buyer’s long-term finances (not immediate needs) and they directly lower the recorded value of the sale.

Now, let’s illustrate these differences with some easy math so you can see the practical impact side by side.

Imagine you’re selling a luxury home listed at $1,200,000. After some negotiation, the buyer is requesting some help to make the deal work. You have two options on the table:

Option A: Provide a $25,000 Seller Credit (keeping the purchase price at $1,200,000).

Option B: Reduce the Purchase Price by $25,000 (to a new price of $1,175,000) with no credits.

Let’s compare the outcomes for both you and the buyer under each scenario:

Sale Price (Comps): In Option A, the contract price remains $1.2M. In Option B, it becomes $1.175M. So, Option A preserves a higher comp for the neighborhood (a plus for you and local home values), whereas Option B sets a new lower benchmark.

Buyer’s Down Payment: Suppose the buyer is putting 20% down. In Option A, 20% of $1.2M is $240,000. In Option B, 20% of $1.175M is $235,000. So with the price reduction, the buyer needs $5,000 less in down payment. Not a huge difference given the scale of the purchase.

Buyer’s Loan Amount: In Option A, the buyer’s mortgage would be $960,000 (assuming 20% down). In Option B, it’d be $940,000. The $20k smaller loan in Option B lowers the buyer’s monthly payment a bit. For example, at a 7% interest rate over 30 years, a $960k loan might cost roughly $6,380/month, whereas a $940k loan might be about $6,250/month. That’s a savings of around $130/month for the buyer with the lower price.

Buyer’s Closing Costs: Let’s say the total closing costs (lender fees, escrow, insurance, etc.) amount to $20,000 in either scenario. In Option A, the $25,000 credit fully covers these $20k of costs and even leaves $5,000 that the buyer can use, for example, to buy down their interest rate. The buyer would come to closing with $0 for closing costs (the credit handles it). In Option B, with no credit, the buyer has to pay the full $20,000 out-of-pocket in addition to their down payment.

Interest Rate Effect: Because Option A’s buyer can use part of the $25k credit for a rate buy-down, let’s assume they manage to reduce their mortgage rate from 7.0% to 6.5% using that extra $5k. Now their $960k loan at 6.5% might cost around $6,070/month – that’s about $310 less per month than $6,380 at 7%. Compared to the Option B buyer (who’s at 7% with a $940k loan, ~$6,250/month), the Option A buyer is actually paying around $180 less per month despite the higher loan principal, thanks to the lower rate.

Buyer’s Cash to Close: Adding it up from the buyer’s side:

Option A: $240k down payment + ~$0 closing costs (covered by credit) = $240,000 cash needed.

Option B: $235k down + ~$20k closing costs = $255,000 cash needed.

Bottom line: The buyer in Option A brings about $15,000 less cash to the closing table than the buyer in Option B. This is a huge immediate benefit for the buyer using the credit.

Seller’s Net Proceeds: Now let’s look at your side (simplified, not accounting for agent commissions or other selling costs).

In Option A, you get $1,200,000 minus $25,000 that you credited to the buyer. Net = $1,175,000 (before other expenses).

In Option B, you simply get $1,175,000 (the lower price) with no credits. Net = $1,175,000.

These are the same. So purely from a gross sales price perspective, your outcome is identical. You sacrificed $25k either way. The differences lie in those other factors we listed: comp value, commissions on the higher price, tax treatment, etc. On the tax front, both scenarios should be effectively equivalent, as the $25k credit in Option A reduces what’s considered your amount realized from the sale (thus similar to just selling for $1.175M)weloveyourtaxes.com.

Summary of the Example: The seller’s net dollar amount from the sale is the same in both cases, but the buyer’s situation improves much more with the credit. They need far less cash to close and can achieve a lower monthly payment by reducing their rate. The seller in the credit scenario maintains a $1.2M recorded sale, while the price-cut seller shows a $1.175M sale. The trade-off for the credit-seller is paying commission on a slightly higher price (and ensuring the credit is within allowed limits), but in return the pool of potential buyers and the attractiveness of the deal increase substantially.

In real life, not every buyer will run these numbers – but many intuitively understand that “$X towards closing costs” is a big help. The example demonstrates why offering a credit can be a powerful strategy to move a high-value home, especially when market conditions have shifted to favor buyers more (as we saw with nearly half of U.S. sellers offering concessions in early 2025mansionglobal.com).

Deciding between a seller credit and a price reduction isn’t always straightforward. It requires understanding your buyer pool, the current Colorado market dynamics, and how each choice might affect the sale and your bottom line. This is where R Squared Realty Experts becomes your invaluable partner. We specialize in analyzing scenarios just like this with Colorado home sellers – particularly in the luxury segment where every decision is magnified.

When you work with our team, we will:

Evaluate Market Conditions: Is the local market favoring buyers or sellers right now? How common are concessions in your price range at this moment? We use up-to-date data to inform our advice, ensuring you’re neither leaving money on the table nor missing an opportunity to attract the right buyer. Whether it’s a hot Denver neighborhood or a slower market in the foothills, our guidance is tailored to your specific area and price bracket.

Run the Numbers: As we did above, we’ll break down the math for your situation. If a buyer offers X, with Y in credits, what does that mean for you net-net? How might it impact an appraisal? We’ll explain it clearly so you feel confident in the path you choose. Our goal is to maximize your proceeds while facilitating a successful, efficient sale.

Consider Your Tax and Financial Picture: We’ll help you factor in things like capital gains implications (for instance, if your sale will exceed the $500k gain exclusion for a primary home weloveyourtaxes.com, we tread carefully in pricing strategy). While we always recommend consulting a tax professional for specifics, our experience with high-value home sales means we can flag potential issues and coordinate with your financial advisors as needed. The difference between a credit and a price reduction can be nuanced – and we make sure those nuances are accounted for in your decision.

Skilled Negotiation: If you decide to offer a credit, we’ll negotiate the terms smartly – ensuring the credit is used in a way that genuinely helps the buyer (and thus helps the deal close) without unnecessary waste. If a price cut is more appropriate (for example, to hit a key price point that attracts a new set of buyers), we’ll execute that change strategically and market the new price to generate fresh interest. In both cases, we position the concession or reduction as a win-win, so the buyer feels they’re getting a great deal while you are still meeting your financial goals.

Selling a luxury home in Colorado requires a strategic approach. Offering a seller credit versus reducing the price is one of the critical decisions that can influence how quickly your home sells and for how much. As we’ve discussed, seller credits often provide greater immediate benefits to buyers without undercutting market values, whereas price reductions have their own place in certain scenarios. The right choice depends on the context – and making that choice is easier with seasoned experts by your side.

R Squared Realty Experts is here to be that trusted advisor for you. Our deep knowledge of Colorado’s housing and appraisal landscape means we understand the impact of every concession, every price move, and every market signal. We pride ourselves on helping sellers of high-value homes make informed decisions that move their properties efficientlywhile maximizing value.

If you’re considering selling and unsure how to position your home in this market, reach out to any member of R Squared Realty Experts. We’ll guide you through each step – from setting the optimal price to deciding on credits vs. price adjustments – so you can proceed with confidence and success. Together, let’s make the most of your Colorado home sale.

Travis Davis

📱: (720) 202-4419

Ryan DeGering

📱: (303) 257-8474

Rudy Avila

📱: (303) 809-6472

Randy Avila

📱: (720) 935-0248

Contact us to provide an experience unlike others and help you take the stress out of buying and selling your home in the Denver and surrounding area today!